Understanding the Business Interruption Insurance Claims Process: A Comprehensive Guide

In today's ever-changing business landscape, unforeseen events can disrupt operations, resulting in financial losses and potential bankruptcy. This is where business interruption insurance comes into play, offering vital protection against such disruptions. However, understanding the claims process can be complex and overwhelming for business owners.

In this comprehensive guide, we will delve into the intricacies of the business interruption insurance claims process. From filing a claim to the evaluation and settlement stages, we will provide you with invaluable insights and practical tips to navigate this often daunting process. Whether you are a small business owner or a seasoned entrepreneur, this guide will equip you with the knowledge you need to protect your business and ensure a smooth claims experience.

Assessing Eligibility for Business Interruption Insurance

Eligibility for business interruption insurance coverage depends on several factors. Understanding these criteria is crucial before filing a claim. The first step is to determine whether your policy covers the specific event that caused the interruption. Common events covered by business interruption insurance include natural disasters, such as hurricanes, fires, floods, and earthquakes, as well as unexpected incidents like equipment failures or cyberattacks.

When evaluating eligibility, insurers also consider policy requirements. These can include a specific waiting period before coverage kicks in, a minimum threshold for the duration of the interruption, and the need for physical damage or loss. Familiarize yourself with your policy's terms and conditions to ensure you meet the necessary criteria for coverage.

Determining Covered Events

Review your insurance policy to identify the events covered by your business interruption insurance. It is essential to have a clear understanding of the specific incidents that qualify for coverage. Keep in mind that different policies may have varying definitions and exclusions. Consult with your insurance agent or broker if any terms or conditions are unclear.

Evaluating Policy Requirements

Thoroughly review your policy to understand its requirements. These can include waiting periods, duration thresholds, and the need for physical damage or loss. Consider obtaining a copy of your policy's declarations page, which provides a summary of key terms, limits, and conditions. This will help you determine whether your claim meets the policy's eligibility criteria.

Consulting with an Insurance Professional

If you are unsure about your policy's eligibility requirements or need assistance in evaluating covered events, consider consulting with an insurance professional. An experienced agent or broker can help you navigate the complexities of your policy and provide guidance on whether your claim meets the necessary criteria for coverage.

Understanding Policy Coverage and Exclusions

Once you have determined your eligibility for business interruption insurance, it is essential to familiarize yourself with the coverage provided by your policy. Understanding the scope of coverage and potential exclusions will help you navigate the claims process more effectively and avoid any surprises or disappointments.

Business interruption insurance typically covers three main areas: loss of income, additional expenses, and temporary relocation costs. Loss of income coverage compensates for the profits you would have earned if the interruption had not occurred. Additional expenses coverage reimburses you for any extra costs incurred to minimize the impact of the interruption. Temporary relocation coverage helps cover the expenses associated with moving your business to a temporary location during the interruption.

Loss of Income Coverage

Loss of income coverage is one of the primary components of business interruption insurance. This coverage is designed to compensate for the revenue your business would have generated had the interruption not occurred. It typically includes net profits and ongoing expenses that continue even when operations are disrupted, such as payroll, rent, and utilities.

When filing a claim for loss of income, it is essential to provide supporting documentation to demonstrate the financial impact of the interruption. This can include financial statements, tax returns, profit and loss statements, and any other relevant records that illustrate your business's pre-interruption financial performance.

Additional Expenses Coverage

In addition to loss of income, business interruption insurance policies often provide coverage for additional expenses incurred as a result of the interruption. These expenses can include costs for temporary repairs, overtime wages for employees, renting alternative workspace, or leasing equipment to resume operations.

When submitting a claim for additional expenses, it is crucial to maintain detailed records and receipts to support your request for reimbursement. Proper documentation will help substantiate the necessity and reasonableness of the expenses incurred during the interruption.

Temporary Relocation Coverage

In some cases, a business interruption may require you to temporarily relocate your operations to an alternative site. Temporary relocation coverage helps cover the costs associated with moving your business and setting up operations in a new location, such as rent, utilities, and equipment expenses.

When claiming temporary relocation expenses, make sure to provide evidence of the actual costs incurred during the relocation period. This can include lease agreements, utility bills, and invoices for any equipment or supplies required at the temporary location.

Documentation and Record-Keeping

Accurate and thorough documentation is crucial when filing a business interruption insurance claim. The more organized and comprehensive your records are, the smoother the claims process will be. Proper documentation not only helps support your claim but also enables you to present a clear and accurate picture of the financial impact the interruption had on your business.

When it comes to documentation, consider the following key areas:

Financial Records

Maintain up-to-date financial records, including profit and loss statements, balance sheets, tax returns, and bank statements. These documents provide a snapshot of your business's financial health before and after the interruption, helping establish the extent of your loss.

Inventory and Asset Records

Keep detailed records of your inventory and assets, including purchase receipts, invoices, and any appraisals or valuations. These records will help determine the value of any damaged or destroyed inventory or assets and assist in calculating your claim's settlement amount.

Business Continuity Plan

If you have a business continuity plan in place, ensure it is updated and readily accessible. A business continuity plan outlines the steps your business will take to minimize the impact of an interruption and resume operations as quickly as possible. Providing your insurer with a well-thought-out plan demonstrates your commitment to mitigating losses and can positively impact the claims process.

Employee and Payroll Records

Maintain accurate employee records, including payroll information, contracts, and any employment agreements. These records are crucial for calculating the ongoing expenses associated with payroll and ensuring that your employees are compensated during the interruption.

Insurance Policy

Keep a copy of your business interruption insurance policy readily available, along with any endorsements or amendments. Familiarize yourself with the policy's terms, conditions, and coverage limits to ensure you fully understand your rights and obligations.

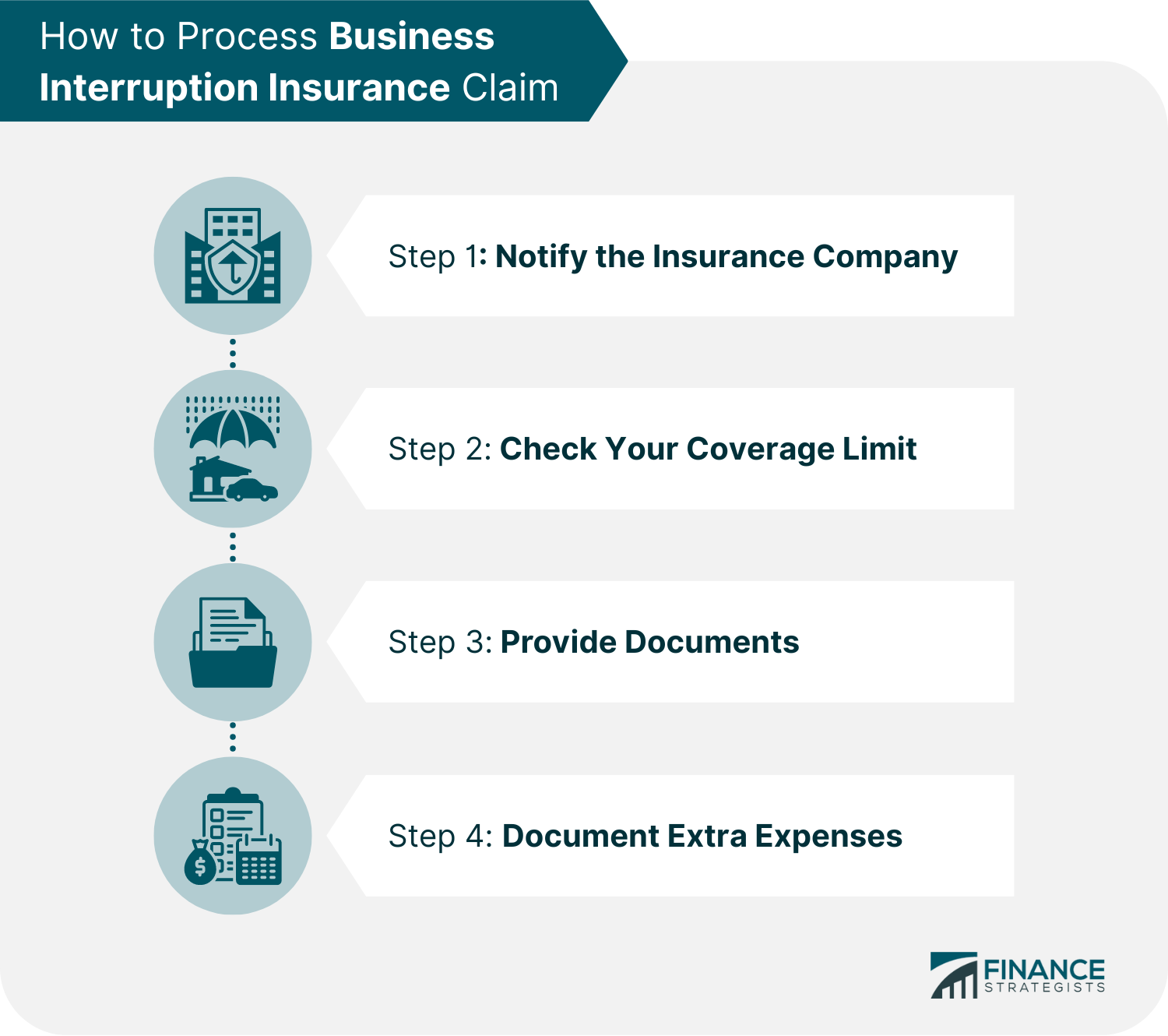

Initiating the Claims Process

Once a disruption occurs, initiating the claims process promptly is essential. The earlier you notify your insurer and begin the claims process, the sooner you can receive the financial assistance needed to recover from the interruption. Follow these steps to initiate the claims process:

Notify Your Insurer

As soon as you become aware of an interruption that may trigger a business interruption insurance claim, notify your insurer. This can typically be done by contacting your insurance agent or broker directly. Provide them with a detailed description of the event and its impact on your business.

Review Your Policy

Thoroughly review your insurance policy to understand the specific requirements and obligations related to filing a claim. Familiarize yourself with any time limits for reporting the loss and submitting supporting documentation. Adhering to these requirements will help ensure a smooth claims process.

Document the Damage

Take photographs or videos of any physical damage to your property or assets resulting from the interruption. This visual evidence can be instrumental in supporting your claim and demonstrating the extent of the loss. Make sure to document all relevant details, including dates and descriptions of the damage.

Complete Claim Forms

Most insurers require claimants to complete specific claim forms to initiate the process formally. These forms typically request detailed information about the interruption, including the date it occurred, a description of the event, and an estimate of the financial impact on your business. Fill out the forms accurately and provide as much information as possible.

Gather Supporting Documentation

Compile all supporting documentation required to substantiate your claim. This can include financial records, inventory lists, employee payroll information, and any other relevant documents demonstrating the financial impact of the interruption on your business. Ensure that all documents are organized and easily accessible.

Claims Investigation and Evaluation

After you file a claim, your insurer will conduct an investigation and evaluation to assess the validity and extent of the loss. The purpose of this stage is to determine the coverage applicable to your claim and calculate the potential settlement amount. Here's what you can expect during the claims investigation and evaluation process:

Initial Assessment

Upon receiving your claim, the insurer will assign an adjuster to handle your case. The adjuster will review the details of your claim, including the event that caused the interruption, the financial impact on your business, and the supporting documentation you provided.

Site Visit and Inspection

In many cases, the insurance adjuster will schedule a site visit to assessthe damage and gather additional information. During the site visit, the adjuster will inspect your property, inventory, and assets, taking note of any visible damage or loss. They may also take photographs or measurements to document the extent of the interruption's impact on your business.

Review of Supporting Documentation

The adjuster will carefully review the supporting documentation you provided, such as financial records, inventory lists, and employee payroll information. They will evaluate these documents to determine the financial impact of the interruption and assess the coverage applicable to your claim.

Interviews and Statements

As part of the investigation process, the adjuster may conduct interviews with key individuals, such as business owners, employees, or witnesses, to gather additional information or clarify any discrepancies. These interviews may be conducted in person, over the phone, or through written statements.

Expert Assessments

In some cases, the insurer may engage external experts, such as forensic accountants or engineers, to provide specialized assessments or evaluations. These experts can help determine the extent of the loss, the cause of the interruption, or the necessary repairs or replacements required to resume operations.

Loss Calculation

Based on the information gathered during the investigation, the adjuster will calculate the loss amount covered by your business interruption insurance policy. This calculation typically takes into account factors such as the duration of the interruption, the financial impact on your business, and the policy's coverage limits and deductibles.

Communication and Updates

Throughout the investigation and evaluation process, the adjuster will communicate with you regularly to provide updates on the progress of your claim. They may request additional documentation or information as needed and address any questions or concerns you may have.

Business Interruption Loss Calculation

Calculating the business interruption loss is a crucial step in the claims process. This calculation determines the amount of compensation you are entitled to under your business interruption insurance policy. The loss calculation involves several key components:

Period of Indemnity

The period of indemnity refers to the duration for which your business is entitled to compensation under the policy. It typically starts from the date of the interruption and ends when your business is fully operational again or when a predetermined period specified in the policy expires.

When calculating the loss, it is essential to accurately determine the period of indemnity, as it directly affects the overall settlement amount. Consider factors such as the time required to repair or replace damaged property, resume normal operations, and rebuild your customer base.

Loss of Gross Profits

Loss of gross profits is a key component in calculating the business interruption loss. It represents the revenue your business would have generated if the interruption had not occurred. To calculate this, subtract the total expenses that would have been incurred during the interruption period from the estimated gross profits.

When estimating the gross profits, consider factors such as historical financial data, industry trends, and any foreseeable changes in market conditions that could impact your business's revenue during the interruption period.

Additional Expenses

In addition to loss of gross profits, business interruption insurance policies often provide coverage for additional expenses incurred during the interruption. These expenses may include costs related to temporary repairs, relocation, equipment rentals, or increased marketing efforts to regain lost customers.

When calculating the additional expenses, gather all relevant documentation and receipts to substantiate the expenses incurred. Ensure that the expenses are reasonable and necessary to minimize the impact of the interruption and restore your business to its pre-interruption state.

Negotiation and Settlement

Once the evaluation is complete, negotiations regarding the settlement amount will commence. The goal of the negotiation stage is to reach a fair and equitable settlement that adequately compensates you for the financial losses suffered during the interruption. Here are some key points to consider during the negotiation and settlement process:

Presenting Your Case

During the negotiation, be prepared to present your case effectively. Provide the insurer with a clear and comprehensive understanding of the financial impact the interruption had on your business. Utilize the supporting documentation you gathered to justify your claim and demonstrate the validity of your loss calculation.

Understanding Policy Limitations

Be aware of the limitations and coverage limits specified in your policy. Understanding these limitations will help you set realistic expectations during the negotiation process. If the initial offer falls short of your expectations, be prepared to provide additional evidence or arguments to support your claim for a higher settlement amount.

Seeking Professional Assistance

If you encounter challenges during the negotiation process or believe that the insurer's offer does not adequately reflect your losses, consider seeking assistance from a professional, such as a public adjuster or an attorney specializing in insurance claims. These professionals can provide valuable guidance and advocate for your interests during the negotiation and settlement stage.

Rejection or Disputed Claims

In some instances, business interruption insurance claims may be rejected or disputed by insurers. This can be due to various reasons, such as policy exclusions, insufficient documentation, or disagreements regarding the extent of the loss. If your claim is rejected or disputed, consider taking the following steps:

Reviewing the Denial or Dispute Letter

Carefully review the denial or dispute letter provided by your insurer. This letter should outline the specific reasons for the rejection or dispute. Pay close attention to the policy provisions, exclusions, or requirements cited by the insurer.

Gathering Additional Documentation

If your claim is rejected or disputed due to insufficient documentation, gather any additional evidence that supports your claim. Consult with professionals, such as forensic accountants or engineers, to provide expert assessments or evaluations that can validate your loss calculation.

Challenging the Decision

If you believe that the denial or dispute is unjustified, challenge the decision by submitting a written appeal to your insurer. Clearly articulate your position, addressing each reason cited for the rejection or dispute. Include any additional evidence or arguments that support your claim.

Engaging Professionals

If the negotiation and appeal process with your insurer proves unsuccessful, consider engaging professionals, such as public adjusters or insurance claim attorneys, to assist you in challenging the decision. These professionals have expertise in navigating insurance disputes and can advocate for your rights and interests.

Timeframe for Claim Settlement

The timeframe for settling a business interruption insurance claim can vary significantly depending on various factors, including the complexity of the claim, the extent of the damage, and the insurer's internal processes. While it is challenging to provide an exact timeline, understanding the general process can help set realistic expectations:

Initial Investigation

The initial investigation, which includes assessing the event, evaluating the documentation, and conducting interviews, can take several weeks to complete. The length of this stage depends on the complexity of the claim and the availability of supporting documentation.

Evaluation and Calculation

After the initial investigation, the insurer will evaluate the claim and calculate the potential settlement amount. This stage can take several weeks or even months, depending on the complexity of the loss calculation and any additional assessments or expert evaluations required.

Negotiation and Settlement

The negotiation and settlement stage can also vary in duration. It typically involves back-and-forth communication between you and the insurer to reach a mutually agreeable settlement amount. This stage can take anywhere from a few weeks to several months, depending on the complexity of the claim and the willingness of both parties to negotiate.

Finalizing the Settlement

Once a settlement amount is agreed upon, it may take additional time to finalize the settlement. This includes drafting the settlement agreement, obtaining necessary approvals, and processing the payment. The timeframe for finalizing the settlement can range from a few days to several weeks.

Maximizing Your Business Interruption Insurance Claim

When it comes to maximizing your business interruption insurance claim, being proactive and well-prepared can significantly impact the outcome. Here are some essential tips and strategies to consider:

Maintaining Accurate Records

Accurate and organized documentation is crucial when filing a business interruption insurance claim. Maintain detailed financial records, inventory lists, and employee payroll information. Regularly update these records to reflect any changes in your business's operations or financial situation.

Implementing a Business Continuity Plan

Having a well-thought-out business continuity plan in place can demonstrate your commitment to minimizing losses and resuming operations quickly. Regularly review and update your plan to ensure it reflects any changes in your business's operations or potential risks. Implementing the plan during an interruption can help mitigate losses and strengthen your claim.

Seeking Professional Guidance

If you are unsure about the claims process or need assistance in preparing your claim, consider seeking professional guidance. Public adjusters or insurance claim attorneys can provide valuable expertise and guidance to maximize your claim's potential and ensure you are treated fairly throughout the process.

Thoroughly Reviewing Your Policy

Before filing a claim, carefully review your business interruption insurance policy. Understand its coverage limits, exclusions, and requirements. This knowledge will help you set realistic expectations and avoid any surprises during the claims process. If any policy provisions are unclear, consult with your insurance agent or broker for clarification.

Engaging in Open Communication

Open and transparent communication with your insurer is key to maximizing your business interruption insurance claim. Keep your insurer informed of any developments or changes in your business's situation, such as repairs, reopening, or additional expenses incurred. Promptly respond to any requests for information or documentation to ensure the claims process moves forward smoothly.

Documenting All Losses and Expenses

To maximize your claim, document all losses and expenses incurred as a result of the interruption. Keep detailed records, including invoices, receipts, and estimates. This documentation will provide evidence of the financial impact on your business and support your claim for reimbursement or compensation.

Considering Business Interruption Contingent Coverage

If your business relies on key suppliers, vendors, or customers, consider adding business interruption contingent coverage to your policy. This coverage protects you if an interruption occurs in the operations of these critical partners, resulting in financial losses for your business. Including this coverage can enhance your claim and provide additional protection for your business.

Engaging in Professional Loss Calculation

In complex cases, consider engaging the services of a professional, such as a forensic accountant, to assist in calculating the business interruption loss accurately. These professionals have the expertise to navigate complex financial calculations and can provide a thorough analysis that strengthens your claim.

Reviewing and Appealing Settlement Offers

When reviewing a settlement offer from your insurer, carefully assess whether it adequately compensates your business for the losses suffered. If the offer falls short, consider appealing the decision and providing additional evidence or arguments to support your claim for a higher settlement amount. Engage professionals if needed to assist with the negotiation and appeals process.

Understanding the Policy Renewal Process

Take the time to review your business interruption insurance policy during the renewal process. Assess whether the coverage limits, exclusions, and deductibles are still appropriate for your business's needs. Consider any changes in your operations or potential risks that may require adjustments to your policy. By ensuring your policy is up-to-date, you can maximize your protection and potential claims in the future.

In conclusion, navigating the business interruption insurance claims process can be complex and challenging. However, by understanding the eligibility criteria, policy coverage, documentation requirements, and the various stages of the claims process, you can maximize your chances of a successful claim. Remember to maintain accurate records, communicate openly with your insurer, and seek professional guidance when needed. With thorough preparation and proactive measures, you can protect your business and secure the financial stability necessary to recover from any interruption.

Post a Comment for "Understanding the Business Interruption Insurance Claims Process: A Comprehensive Guide"